5 Crucial Things You Shouldn't Lie About When Applying for a Mortgage

Space Intown, REALTORS® July 21, 2023

Space Intown, REALTORS® July 21, 2023

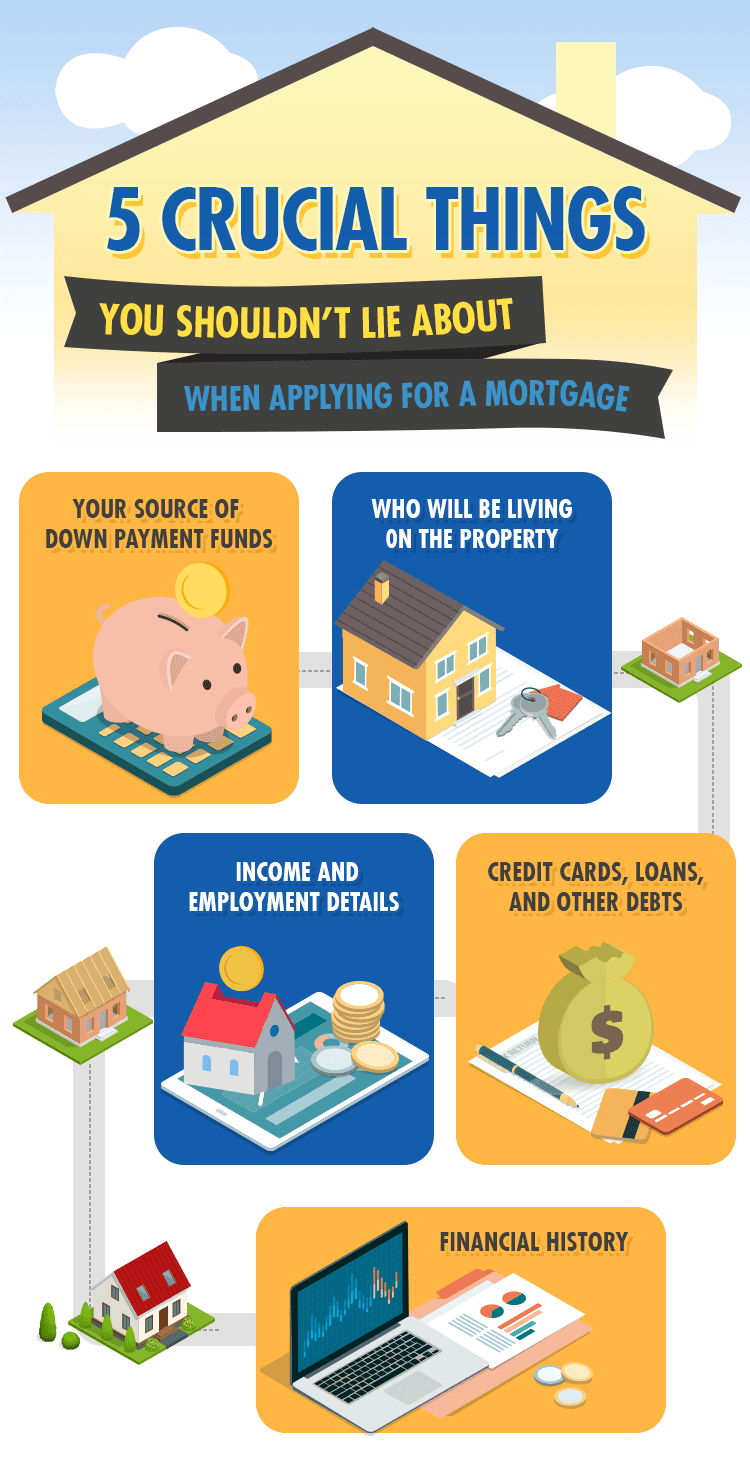

The lender could downright deny your application.

If you’re already under contract, your earnest money deposit could be forfeited.

If the truth comes to light after the deal is done, the lender could decide to call the loan payable. This means you have to pay the full amount of the mortgage, or face foreclosure.

The lender could increase your rate as a penalty, leading to higher interest and monthly mortgage payments.

Worst case scenario: you’ll be charged with mortgage fraud, with a penalty that can include a maximum of 30 years prison time and a $1 million fine.

The biggest lesson: Just be honest from the start so you’ll have a better chance of getting approved for a mortgage.

Condo Living

Learn how condo pet policies, weight limits, breed restrictions, and pet-friendly amenities can influence buyer demand, marketability, and long-term resale value.

Condo Living

Learn how condo insurance works in Georgia, including HOA master policies, HO-6 coverage, loss assessments, liability protection, and what condo buyers should know bef… Read more

Buckhead

Discover Buckhead's favorite brunch destinations, from French-inspired cafes and rooftop patios to Southern comfort food and neighborhood favorites. Perfect for buyers… Read more

Atlanta Neighborhoods

Explore 15 of Atlanta's most walkable neighborhoods, from Midtown and Inman Park to Virginia Highland, Decatur, Buckhead Village, and more. Perfect for buyers seeking … Read more

Atlanta

Discover what it's really like to live in Midtown Atlanta with this ultimate weekend guide featuring Piedmont Park, the BeltLine, local dining, arts, and luxury condo … Read more

Atlanta

Discover the most walkable neighborhoods in Atlanta, including Midtown, Inman Park, Virginia Highland, Buckhead Village, Old Fourth Ward, and Decatur.

Atlanta Neighborhoods

Thinking about buying your first home in Inman Park? Learn what to expect, from housing options and BeltLine access to budgeting tips and navigating this competitive A… Read more

Atlanta Neighborhoods

Thinking about moving to Brookhaven? Learn what it's like to live in one of Atlanta's most desirable neighborhoods, from housing and parks to dining and commuting.

Real Estate 101

Thinking about selling your Brookhaven luxury home? Learn why late summer can be a strategic time to list and what today's luxury buyers are looking for in Atlanta.

Do you have inquiries about the real estate process? Need expert advice on a property? Interested in exploring investment opportunities? Our team is here to provide the answers you seek. Contact us today; we'll be delighted to assist you and offer expert guidance, helping you navigate Atlanta's real estate landscape with confidence.